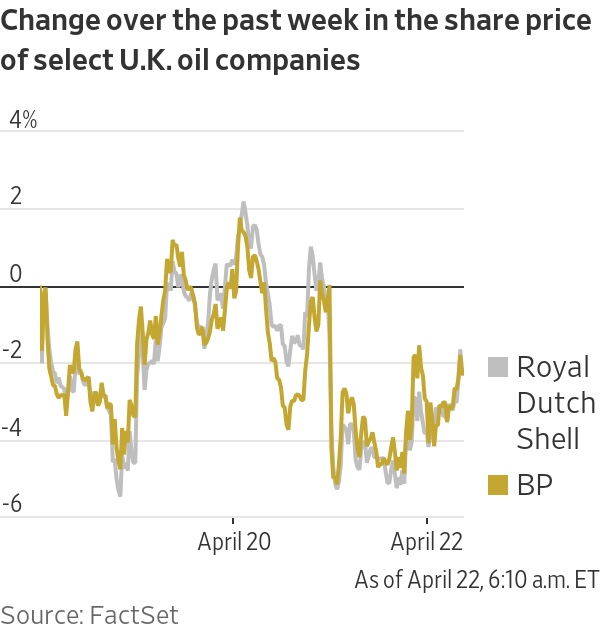

The recent fall in the value of oil has reverberated across energy markets, hitting the value of oil companies

By David Hodari and Caitlin Ostroff

Updated April 22, 2020 3:31 pm ET

Crude prices rose Wednesday, pausing a weekslong crash after President Trump warned Iran that he has instructedthe U.S. Navy to destroy Iranian gunboats if they continue to harass American ships in the Persian Gulf.

U.S. crude-oil futures for delivery in June rose 19% to $13.78 a barrel, extending a series of chaotic moves. The most heavily traded U.S. crude benchmark on Tuesday collapsed to a 21-year low, with supply overwhelming demand and storage in many parts of the world full.

On Monday, a U.S. crude futures contract turned negative for the first time ever, effectively meaning sellers were paying buyers to take away oil due to a lack of storage. The contract that turned negative early in the week expired in positive territory on Tuesday.

Brent crude futures, the global benchmark for oil markets, climbed 5.4% to $20.37 a barrel on Wednesday but also remained near a multidecade low.

The president’s warning on Twitter to Iran helped spur the gains and followed recent encounters between U.S. ships and Iranian vessels. The possibility of tension in the region can boost oil prices by signaling potential disruptions to shipments of oil around the world and possible supply shortages.

Still, many analysts expect the glut of crude that has collapsed prices to persist due to the coronavirus pandemic.

“It’s a geopolitical piece of news that has lifted the price at a time when the market has been heavily sold,” said Ole Hansen, head of commodity strategy at Saxo Bank.

That came two days after one WTI contract turned negative for the first time in history, with sellers paying buyers to take away their barrels.

While benchmark oil-futures prices have collapsed this week, the price of a physical barrel of oil is even lower. A real-life barrel of Brent crude oil cost $13.24 late Tuesday, its lowest price since March 1999, according to S&P Global Platts. Physical prices in some parts of the U.S. have recently turned negative.

This week’s crushing fall in the value of oil has reverberated across energy markets, hitting the value of oil companies and the debt they issue. If oil prices stay at such a low level, the loss of revenue is likely to create widespread financial and political pain for countries reliant on petroleum production.

Government measures keeping billions of citizens at home in an attempt to stymie the spread of the coronavirus have decimated oil demand. Compounding the problem was a massive overproduction of crude during a price war last month between Saudi Arabia and Russia.

The two sides have called a truce, but now the world is essentially swimming in oil that nobody needs. Some oil producers have been reluctant to shut down because doing so quickly could cause long-term damage to their wells.

Storage capacity has appeared to reach its limit, prompting this week’s massive selloff.

“We could see unexpected methods of storage coming into play if they can’t store it in the traditional pipeline system,” said Richard Fullarton, founder of London-based private fund manager Matilda Capital Management Ltd. “They may have to store it in on-land pond facilities or cap a whole tranche of wells.”

Industry data have underscored the massive oversupply. Government figures Wednesday showed U.S. stockpiles rose 15 million barrels last week, extending a recent stretch of sizable increases.

Free commercial oil storage capacity has dwindled to around 130 million barrels out of an estimated 1.38 billion barrels of space, according to cargo tracker Kpler, although logistical bottlenecks mean not all that capacity can be used.

The shock to oil prices has reverberated through broader markets, sending stocks of oil producers down. Debt issued by energy companies also has sold off sharply, indicating the rising risk of a wave of defaults, something that could affect other high-yield borrowers, said Seema Shah, chief strategist at Principal Global Investors. U.S. oil companies are among some of the largest issuers, making up about 12% of high-yield bond indexes.

“With oil prices so low, they are going to be under so much pressure right now that you almost have a contagion effect from energy to high yield,” she said.

Shares of energy producers also rebounded Wednesday, with some large companies like BP PLC rising 5% or more.

“There’s a very significant contrast between low oil prices and high equity prices, and I think this has been a reminder that we’re not in the clear yet,” Ms. Shah said. “At least in the short term oil prices are going to be under pressure,” she said.

The drop in prices will most hurt countries that depend on oil for much of their revenue, according to Chris Turner, head of foreign-exchange strategy at ING Bank. Countries including Iraq and Bahrain rely on oil for most their revenue, according to an ING analysis.

The Forces Fueling 2020’s Oil Bust

—Joe Wallace and Amrith Ramkumar contributed to this article.

Write to David Hodari at David.Hodari@dowjones.com and Caitlin Ostroff at caitlin.ostroff@wsj.com

No comments:

Post a Comment